Chief Currency Strategist at KSHITIJ.COM. Likes to look at the markets from many different angles. Weaves many conventional and unconventional technical analysis techniques and fundamental analysis into a global macro perspective. Likes to take the road less traveled.

The general market sentiment is very bullish on Gold right

now, with people looking for 2000$+ levels and Ray Dalio’s article on Linked

adding to the sentiment.

But, we want to share with you reason why Caution on Gold

may be good.

Today is 26th July 2019, Gold is at $1418 and I am Vikram

Murarka.

This video is a little long, but it might be worth your

time. So, here goes…

Slide 2

True to its nature as a safe haven, the rise in Gold since

May 2019 has been on the back of global tensions.

The left axis shows weakness in Yuan due to US-China trade wars.

The right axis shows strength in Gold in the same period due to the US-China

trade wars and US-Iran tensions.

It is said that the Chinese central bank has bought Gold in

this period, but we would not lay too much store on that. I will show you why

in the next slide.

Basically, the rise in Gold since May seems to be driven by

news rather than value.

Slide 3

Let me show you the BIG picture in Gold, since 1836.

The upmove from $21 in the 1870-1930 period to $1921 in 2011

mave have completed a 5-wave sequence.

Wave 1 – Gold rose with WWI

Wave 2 – We take this period of stability as Wave 2

Wave 3 – started with the US

breaking the Gold Standard in 1971 and ended with the Soviet invasion of Afghanistan in

1979-80.

Wave 4 – saw Gold come down to $272 in 2001, where the Bank

of England famously sold its Gold reserves. That is why I am not very taken in

by central bank action on Gold.

Wave 5 – saw Gold rising with the global commodity boom and

Dollar weakness, culminating at 1921 in 2011.

Now we are possibly seeing a small A-B-C correction, where A

has already happened. The current rally might be B and may end anywhere now, on

this Moving Average resistance. A wave C (yet to happen) may bring the Log

Chart down to 6.90, which would translate to $992 on Gold.

Slide 4

This is a very important chart, showing a very strong

correlation between Gold and Crude since 1861.

And, regular clients know that we are bearish on Crude,

targeting $33 by 2020-2021. Therefore, if the correlation holds, Gold too may

come down towards $992.

Slide 5

Here is more medium term chart on Gold.

Here too, we see that the upmove since 1170 in Aug-18 may

itself have been a 5-wave upmove, which might have got completed at $1454 in

July.

Slide 6

Looking at a slightly bigger picture, we see that $1483 is

the 50% Fibonacci retracement of the fall from $1920.70 to $1045.40. Also, we

have a trendline Resistance at $1500 here.

So, there is a decent chance that Gold may either have

topped out at 1454 itself, or might top out anywhere in the 1483-1500 region.

And now comes the really interesting part.

Slide 7

This chart shows the dramatic underperformance of Gold

vis-a-vis the Dow Jones, clearly showing how Equities have been a better

investment than Gold.

And, this underperformance is still very much in force. The

Gold/ Dow ratio faces an important Resistance right here. If and while this

holds, Gold can fall again.

Of course, the Resistance could break as well. But, then we

would want to buy Gold only if we see clearly that the Resistance has broken.

Not before.

Slide 8

Not only has Gold underperformed the Dow Jones, it has

underperformed the Sensex as well.

And it faces a crucial Resistance right here, coming from

2007.

So, again, we cannot buy Gold unless this Resistance is

broken.

Slide 9

Gold also faces Resistance against Copper right here. In

fact, if the Gold-Copper ratio comes down, it might be good for Equities as

well, as fear goes out of the market.

Slide 10

Gold has a good Resistance against Crude as well, and this

is, in fact, a pretty strong Resistance.

Slide 11

And lastly, Gold is just coming off a Resistance right here

on the MCX in India,

one of the largest markets for Gold.

So, not only does Gold have Resistances on its own charts,

it does not seem to be a value buy against 5 other markets.

This makes us very cautious about becoming bullish on Gold

at current prices.

Slide 12

And, if the Resistances that we have pointed out hold, then

Gold could come down towards $1360 or even $1300 by December.

Any positive news on the US-China trade front could be a

positive trigger. On the other hand, fresh deterioration in the US-China or

US-Iran situation could lead to the Resistances breaking. That said, the charts

suggest greater chances of positive news and Gold coming down towards

$1360-1300.

It may/ may not rise again from the $1360-1300 region. But,

if the very long-term reading is correct, there may also be chances of seeing

$992 by 2020-2021.

Let us see now that goes.

Slide 13

For now, those were the reasons why we think Gold does not

glitter at current levels.

NOTE 1: This is not a strictly predictive report. This is more of an exploration of possible multi-decade trends for Dollar-Rupee. It aims to lay out two main possibilities (of either Rupee strength towards 60 against the US Dollar, or weakness towards 172) before policy makers; and to suggest that we, as a country, should choose the path of Rupee strength.

NOTE 2: As per our analysis in Chart 6a and Chart 6b herein, the post-Independence rise in USD-INR might have already gotten over at 74.4825 in Oct-2018. The validity of this analysis hinges on the acceptance of a particular rare phenomenon. We are accepting this rare phenomenon because

(A) acceptance thereof allows the Rupee movement since 2008 to fit in with some other movements in the global currency market and (B) although rare, the phenomenon cannot be rejected (a bit like, although rare, a white peacock is accepted as a peacock, not rejected.)

NOTE 3:We are sharing this analysis because (A) we sincerely believe it has merit and (B) there is a very important policy implication to be considered at the highest level (please refer Note 1 above).

NOTE 4:There is a 30-50% chance that our analysis is wrong. But, there is also a 50-70% chance that the analysis is right. Even if the analysis is wrong and USDINR has not already seen a top at 74.4825 in Oct-2018, there is a very good chance (near 70%) that the post-Independence weakness of the Rupee can naturally come to an end anywhere between 75-77. That is, if the economic orthodoxy of the authorities does not stand in the way and disrupt the natural movement of the USDINR.The alternative would be to see Rupee weakness continue into perpetuity.

As the origin of the word itself suggests, Economics has concerned itself with the distribution of limited resources. The evolution of Economic theory has reflected the evolution of the human economic experience over time of what limited resources means.

Given that after the Greek and Roman eras, Western thought emerged only in the Renaissance after the struggles for survival through the Dark Ages and bloody wars through the Middle Ages, it is no surprise that the Western philosophers took a rather dim view of the world. So we have Thomas Hobbes (1588–1679) calling life “nasty, brutish, and short”. Quite understandably, therefore, the worldview of the Classical economists was centered on the concept of limited resources. Hence the choice of the word “economics”.

In contrast, India, the land of milk and honey since as far back as human history goes, never experienced any material shortages before the white man came in. However, that is a different line of thought and I should not digress so early in my ramblings.

Coming back, the central concept of limited resources was reflected in the inflexible and vertical Long Run Aggregate Supply (LRAS) curve of the Classical Economists. With time, theory evolved to the point where Keynes depicted the AS (aggregate supply curve) as horizontal at lower levels of GDP before it curved up to become vertical at higher levels of GDP. This small video from Khan Academy is a nice primer on this. With this, there were two important transitions in economic thought that happened. Firstly, with the change in the shape of the AS curve, the productive capacity (or AS) was no longer seen as a major limiting factor on the economy. Secondly, the focus shifted, instead, to AD (aggregate demand) being seen as a limiting factor on the economy. Today, with a globalised economy and globalised supply chains, if anything, the developed world (certainly) finds itself dealing with the problem of more than ample supplies and less than adequate demand.

Keynes onwards, it is the non-availability of Money (as a means of exchange), that has been seen as the factor that constrains demand. No money, can’t spend. So, in the beginning, the government was allowed to run a deficit. Later, the Gold Standard was abandoned by Nixon in 1970 and the USA was free to print as many Dollars as it wanted, unencumbered by any obligation to moor the Dollar to its Gold reserves. While there might be a tendency to baulk at this, we have to concede that these two developments have been crucially vital enablers for the post-War global economic growth and for the post-1970s globalization which has helped billions to come out of poverty, a process that still continues.

More recently, only the most churlish will refuse to admit that had Helicopter Ben not invented QE (quantitative easing) and had Draghi not done “what it takes” after the Great Financial Crisis of 2008 and the European Crisis soon after, the developed world would have had to go “back to the future” to the Great Depression. These two keen students of Keenes (oops, Keynes) freed central banks from the obligation to link money supply to any fiscal considerations.

Today, with the advent of the coronavirus crisis, the world is willing to run up huge deficits in order to send cheques to everyone as everyone is being forced to work from home as country after country and economy after economy goes into lockdown. Western thought has come a long way from the time when Marie Antoinette said “If they don’t have bread, let them eat cake” to the time today when Trump is willing to say “Let us give them bread (cash) so that they can eat cake”.

Welcome to the emerging world of Modern Monetary Theory (MMT) which cites Japan as an example and says there is no reason why governments cannot run deficits that are several times the size of their GDPs. Listen to Stephanie Kelton, one of the champions of MMT, explain this theory. Notice that inflation is no longer a monster to be scared of. Supply not being a constraint, Demand-Push Inflation is dead. Further, with Crude now likely to stay well below $70 for some years ahead and to be eventually replaced by solar power, Cost-Push Inflation may also be a demon that might get slain. In this environment, when government bond yields are headed towards zero and are likely to stay there for years together, why should not governments run unlimited deficits?

There are merits to this evolution of thought that says non-availability of money should not be allowed to constrain demand. If governments do not have money, they can run deficits. If central governments need to expand money supply, they may simply create. Human population has grown and everyone is seen to have a right to not only the minimum of roti-kapda-makan, but also to education, holidays, smartphones and Netflix. Is there any philosopher or politician anywhere in the world with the gumption to deny this? If people do not have money, they should be given money. Today the daily wage earner (whether in the United States or in Uttar Pradesh) should be given money due to the coronavirus. Tomorrow it will be given as a part of Universal Basic Income. At no point of time should peoples’ demand be curtailed and the wheels of commerce should not grind to a halt due to the non-availability of money.

Or, how India/RBI’s policy of weakening the Rupee to promote Exports does not work and can actually harm Investments, Exports and Growth.

Also, the global markets are presenting us with a unique opportunity. We should take it.

26-Jun-20, USDNR @ 75.63

Executive Summary

India/RBI has long followed a policy of weakening the Rupee, ostensibly in an attempt to promote Indian exports and thereby reduce the country’s chronic trade deficit (hereinafter referred to as “the policy”). [Ref I, II].

Several studies have conceded that a weakening currency does very little to promote exports growth, yet we persist with the policy. Alarmingly, not only has this policy not delivered export growth, it now threatens to severely damage India’s ability to raise foreign capital that is so vital for the massive investments that the country needs.

Further, since August 2019, the RBI is actively creating a one-way-street in the forex market, where only Rupee depreciation is allowed, not Rupee appreciation. This can have disastrous results in that, if pushed beyond a point (which is very close by), the Rupee could weaken by 126% over the next decade. The situation is dire and there is very little room for policy error here. The RBI would do well to forthwith abandon its old policy of weakening the Rupee in a one-way manner and leave the exchange rate to its own devices, else it could be courting disastrous consequences.

Ironically, the global market conditions are currently presenting India with a unique never-again opportunity to enter into a virtuous cycle of strong/ stable currency – higher investments – higher exports – higher growth, all with lower inflation and lower interest rates. This can either be capitalized on by leaving the exchange rate alone, or it can be frittered away by engineering perpetual Rupee weakness, with disastrous consequences.

IV. Rupee weakness can impede Investments – warning from the Sensex V. Impairing the market’s shock absorbing capacity

Section C: The Future Outlook

VI. Opportunity presenting itself – should be capitalized on VII. A bright future is possible. Please do not commit Hara-kiri. VIII. Progression or Regression – two possibilities

APPENDIX: China and Japan: Currency and Exports have weak correlation References and Data Sources

Ref I. Yin-Wong Cheung and Rajeswari Sengupta: It is perceived that the Reserve Bank of India adopts an asymmetric intervention policy that stems a currency appreciation whereas allows a reasonable amount of depreciation.

Ref II C. Rangarajan & R. Kannan: The stated policy of the Reserve Bank is that it has no specific target and that it intervenes only to reduce volatility. This is only partially true.

SECTION A – EVIDENCE REFUTES POLICY

I. FX Rate does not influence Exports, nor does it impact Imports

Contrary to popular belief that a weakening currency leads to exports growth, data and research [Ref I, III] show that this is not so. Rather, the opposite correlation seems to hold truer in India since 2000.

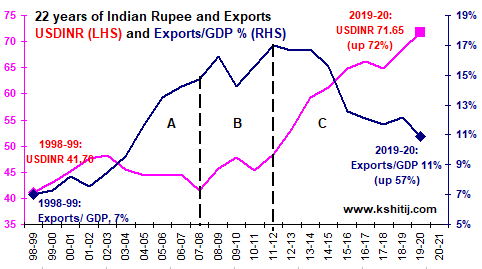

Fig 1: 22 years of USDINR and Exports/ GDP

The USDINR (left axis) has weakened 72% from 41.70 in 1998-99 to 71.65 (average) in 2019-20.

In this period, Exports/ GDP (right axis) has risen only 57% from 7% in 1998-99 to 11% in 2019-20. This period can be divided into sub-periods A, B and C. Periods A and C show that the policy in question does not work.These are examined below.

Table 1: USDINR and Exports/GDP movement in India

It is only in Period B (a short interlude of 3 years from 2008 to 2011) that the theory seems to work. In the longer timeframe of Period A (8 years) and Period C (9 years), export performance is actually seen to be contrary to what might be expected if the theory were correct.

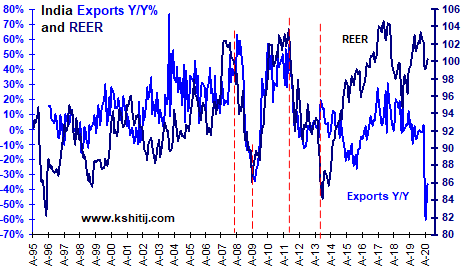

Fig 2: REER also does not work

India’s annual Exports growth (left axis) showed steady improvement since 1996, more so after 2000. During the period, the Real Effective Exchange Rate (REER, right axis) went from an undervalued level of 82 to an overvalued level of 102. Later, even as the REER became undervalued, exports fell and again thereafter, even though the REER became overvalued, exports rose. If anything, the REER and Exports correlation is opposite to that expected as per theory. [Ref I]

Ref I. Yin-Wong Cheung and Rajeswari Sengupta: …starting from 1993-94 onwards, the expected relationship seems to have been reversed… Indian exports grew rapidly since 2000 despite the REER appreciation…

Ref III. Spyros Roukanas, Persefoni Polychronidou, Anastasios Karasavvoglou: Statistical data on real effective exchange rate and aggregated data of Serbian exports indicate that the ambience of overvalued national currency did not harm export performance.

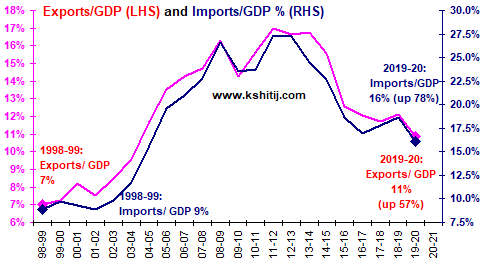

One might think that perhaps the exchange rate policy is expected to curb the trade deficit by curbing Imports. After all, a stronger Rupee (2001-08) was accompanied by higher Imports and later a weaker Rupee (2011-20) saw a fall in Imports. However, this behaviour of Imports is because it has a symbiotic relationship with Exports, as seen below.[IV]

Fig 3. Exports and Imports move together

Exports and Imports move up and down together closely. This is because (a) over the years, the import content of India’s exports has risen and (b) both exports and imports are impacted more by the global trade climate than by the exchange rate.[Ref II]

This relationship between export-import is observed in China and Japan also.

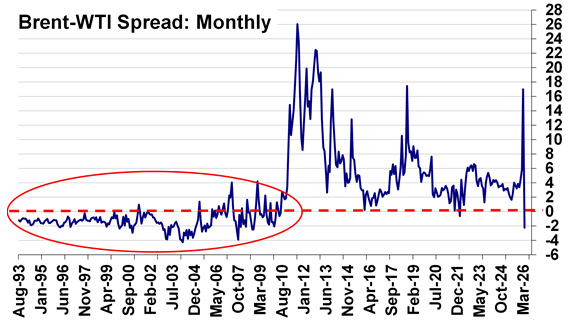

Fig 4. Exports and Imports move with Brent prices

We just saw how Exports and Imports move together. Here, we see that, As might be expected, India’s Imports and Brent Crude prices increase/ decrease together.

Therefore, India’s Exports, Imports and Brent Crude prices all move together.

This is because Crude prices can be taken as a barometer of global trade and GDP growth and it is this which impacts Indian exports/ imports more rather than the Dollar-Rupee exchange rate. [Ref II]

From the evidence so far, we can surmise that the policy of weakening the Rupee to promote Indian exports and narrow the trade deficit has not worked.

Ref II: C. Rangarajan & R. Kannan: The import content of India’s exports has risen from 9.4% in 1995 to 24% in 2011; we find that World Exports has a more powerful effect in influencing exports than REER. World Exports account for 83% of the variability as against 17% of REER

II. Exports respond to Investments, rather than to the Rupee

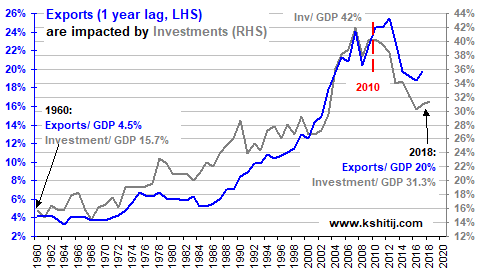

It is well known that Exports are positively impacted by investments in infrastructure (ports, roads, power et al) and production capacities (large scale factories), because these go much further in enhancing a country’s export competitiveness in the world market rather than a weakening currency. The data bears this out.

Fig 5. Exports are related to Investments

As Investment/ GDP grew from 15.7% in 1960 to 42% in 2007, Exports/ GDP also rose from 4.5% to 21%.

In this period also, investments grew faster from 1984 to 2007 as compared to earlier, and exports also picked up speed in line with investments.

After 2010, the Inv/GDP ratio fell to 31.3% and along with it, Exports/ GDP also fell to 20%.

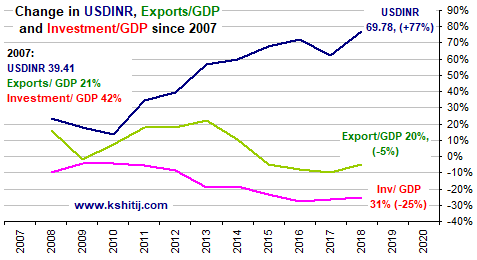

Fig 6. Rupee weakened 77%, yet Exports fell 5%

This chart zooms into the period after 2007.

We find that by 2018, the Rupee had weakened 77% compared to 2007. Yet, in this period, Exports fell by 5%. This again clearly shows that the exchange rate has no impact on Exports.

Rather, Exports fell in line with the 25% decline in the Investment/ GDP ratio.

Exports competitiveness and growth in the world market is a complex thing. It depends on a number of factors including infrastructure, quality, global demand, marketing, research and development, enabling legal system, labour productivity, economies of scale and so on. It is simplistic to think that Export growth can be increased by weakening the currency. If anything, it is better to aim to promote Investments as a means to achieve Exports growth. [Ref II]

We should be warned that weakening the Rupee in pursuit of an empty theory can jeopardize Investments, the single most important factor contributing to higher exports and GDP growth. The exchange rate may be left to its own devices.

Ref II: C. Rangarajan & R. Kannan: Truly speaking, the critical factor is not so much exchange rate as competitiveness… the exchange rate variable represents more than the pure exchange rate. It really stands for the degree of competitiveness of Indian exports… The crucial factor is not so much exchange rate as competitiveness. The whole gamut of policy measures government introduces from time to time are aimed at this objective. We have not been able to take into account explicitly this factor. Exchange rate is one element in this basket of measures.” [Author’s observation: inability to measure the competitiveness of Exports and positioning the exchange rate as a proxy for it is leading to a grave policy error, which should be stopped forthwith].

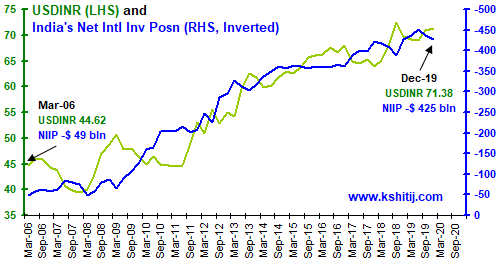

III. IIP and FX Reserves – another albatross around the Rupee’s next

Another argument put forth to support the policy of weakening the Rupee is that the RBI needs to build its FX Reserves as a counterbalance to India’s Net International Investment Position.

Fig 7.Weakening the Rupee with NIIP

India’s NetInternational Investment Position (NIIP, right hand axis, inverted) has “deteriorated” since 2008 as India’s economy has been increasingly opened to international capital flows. As can be seen, the Rupee has weakened alongside.

In a manner, a deteriorating NIIP can be seen as a “risk” and a cause for concern. However, it is a given that the NIIP will continue to “deteriorate” over time, as India’s need for foreign capital will only keep on increasing and that FX Reserves will never catch up or limit the growth of the NIIP. If the RBI continues to buy Dollars to increase FX Reserves “war chest”, then the Rupee can weaken into perpetuity.

Increased Dollar buying since Aug-2019. Why?

The RBI has significantly increased its Dollar purchases since August 2019 [See Section B-V], forcibly preventing Rupee gains even in the face of robust capital inflows. While RBI purchasing Dollars is not new, what we now see is that the RBI is intervening not to smoothen out volatility but to actively prevent Rupee appreciation. This is a new phenomenon and seems to be somehow linked to the adoption of the new Economic Capital Framework (ECF) after Aug-2019, although we do not clearly understand how and why.

FX Reserves form 73% of the RBI’s balance sheet. To quote from the August 2019 report of the Expert Committee to review the extant ECF, “… the RBI suffers losses when the rupee appreciates against the USD and/ or the other currencies in its forex portfolio and it gains when the rupee depreciates against them.Thus, counter-intuitively, the RBI suffers valuation losses during times when the economy is witnessing strong growth and large capital inflows which normally are associated with rupee appreciation.”

The accumulated revaluation profits over the years makes up the Revaluation Reserves of the RBI. By including this in the Contingent Risk Buffer (CRB) of the RBI, the CRB stood at 26.8% of the RBI’s balance sheet (on 30-Jun-18), well in excess of the 6.5% level recommended to meet various risks faced by the RBI. Excluding the Revaluation Reserves, the CRB stood at 7.2%, still in excess of recommended 6.5%.

The Expert Committee to review the extant ECF has recommended that the Revaluation Reserves should be retained with the RBI and should not be alternatively deployed or distributed (say by way of dividend to the Government). It is perplexing then, as to why the RBI is continuing to increase its Reserves.

The only explanation seems to be that apart from the possibility that it wants to avoid revaluation losses due to Rupee appreciation (?), it also seems that it is acutely sensitive to “financial stability risks”, especially after the GFC. In the words of the Expert Committee, “financial stability risks are those rarest of the rare, fat tail risks whose likelihood can never be ruled out and whose impact can be potentially devastating.”

The question that arises is, could the dogged building up of Reserves as a foil against such risks actually end up inviting the far away risk closer, so close that it actually materializes? The danger is that Rupee weakness beyond ………

Those include global currencies (Euro, EM Currencies etc), equities (Dow Jones, MSCI EM indices etc), commodities (Gold, copper, oil etc), bonds (US Treasury, TED Spread etc) and fundamental data.

Correlation studies and inter-market relationships also form a major part of our analysis.

The extensive study we do on all these factors helps us gauge where the Rupee is going, but we don’t stop here. We also record all our forecasts and conduct performance reviews in order to make continuous improvements and minimize errors in what we do.

Over the years, many of our clients have asked us why, when we publish forecasts, sometimes we predict the direction of the movement correctly, the timing of our prediction is incorrect.

Here, we wish to provide some clarity in that regard.

Some of the basic tools that we at Kshitij use in our charts for our analysis are: 1. Trendlines 2. Candles 3. Moving Averages 4. Line Charts Most of our charts are very simple with only the above mentioned basic tools. We do not use many oscillators or momentum indicators either.

Through our currency forecasts and hedging strategies, we like to think that we provide a sense of reliability to our clients. This is most manifest in the 14-year track record of our Dollar-Rupee forecasts, the first, and to our knowledge, still the only one of its kind in India, which proves in real, verifiable numbers, a reliability of 74%.

Rupee Forecasting – Advanced Techniques – The KSHITIJ Way

To see where the Indian Rupee is going we look at 50 factors. Yes, you read it right, 50 factors. Those include global currencies (Euro, EM Currencies etc), equities (Dow Jones, MSCI EM indices etc), commodities (Gold, copper, oil etc), bonds (US Treasury, TED Spread etc) and fundamental data. Correlation studies and inter-market relationships also form a major part of our analysis. The extensive study we do on all these factors helps us gauge where the Rupee is going, but we don’t stop here. We also record all our forecasts and conduct performance reviews in order to make continuous improvements and minimize errors in what we do.

In our last report (27-Feb-26, UST10Yr 4.01%), which was published just one day before the start of the US-Israel-Iran War on 28-Feb, we had continued to target 4.60% on the US10Yr based on expectations of higher Crude. At that time, we were looking for Brent to rise …. Read More

WHAT'S NEW?

Apr’26 Crude Oil Report

The escalation of war between US and Iran throughout March-26 has led to a rally in Brent prices to as high as $119.50, exceeding our bullish targets by a large margin, much ahead of expected time. Will it remain bullish for the coming years?… Read More

WHAT'S NEW?

Mar’26 EURUSD Report

Our view of a fall towards 1.14 seems to be playing out well so far as the tensions in the Middle East and the US-Iran conflict have triggered a rise in Dollar Index and crude oil prices, thereby weakening to Euro to 1.1507 so far in Mar-26. Will it again attempt to rise targeting 1.20? Or will it remain below 1.19/20 now and see an eventual decline to 1.10? …. Read More

WHAT'S NEW?

Apr’26 GOI Report

In our 09-Mar-26 report (10Yr GOI 6.69%) we had warned that the sharp rise in crude due to the US-Iran conflict could push Brent toward $134, which would lift CPI toward ~6.2%, eliminating any chance of RBI easing, and potentially force tightening. This inflation shock, along with higher US yields, was expected to push the 10Yr GOI up to … Read More

WHAT'S NEW?

Jan’26 USDJPY Report

In our 10-Dec-25 report (USDJPY 156.70), we expected the USDJPY to trade within 154-158 region till Jan’26 before eventually rising in the long run. In line with our view, the pair limited the downside to … Read More