Chief Currency Strategist at KSHITIJ.COM. Likes to look at the markets from many different angles. Weaves many conventional and unconventional technical analysis techniques and fundamental analysis into a global macro perspective. Likes to take the road less traveled.

August 2018 has been a trying time for Importers because Rupee has depreciated to its weakest ever level of 70.39. In this video we show how our Reliable long-term Dollar-Rupee forecasts and systematic hedging over the past 12 months have helped save Rs 1.54 per Dollar.

This saving could have been possible only when there is a combination of

Yes, it is true. Like in all other important aspects of life, in forex hedging also, size indeed matters.

Remember that old formula, R = p.q, or Revenue (or Outgo) = Price x Quantity?

The successful businessman keeps an eye on both variables, whether he is selling or buying. Depending on the nature of price movements in the market he is operating in, monitoring the quantity becomes less or more important. If the price tends to be fixed, then the only thing to do to maximise revenue is to try and maximise the quantity.

However, if there is a fairly large degree of variability in the prices, then it becomes very important to judiciously increase/ decrease the quantity transacted at each different price with the aim of maximizing the sale revenue or minimising the purchase outgo.

The same simple concept applies to successful forex hedging as well, except that most of the time our attention is so fixated on the Price (rate) only, that we tend to totally forget the importance of the Quantity (amount) part of the equation. Picture the professional card player. He keeps varying the amounts that he bets.

When we do that, we equip

ourselves with a variable (Amount) that we have greater control on that the

Rate. If the rate is not very attractive but we are compelled to hedge, we can

look to reduce the amount. If the rate is good, we can increase the hedge

amount.

Further while the difference between two hedged rates tends to vary by 1-5%, the amount that is hedged tends to be in the region of 8-20% of the exposure amount and should therefore actually have a greater weightage in the R = p.q. formula.

Taking another analogy, while

driving, all of us regularly use the accelerator also (apart from the brake) to

reduce speed, perhaps more often than the brake. Imagine what would happen if

we were to use only the brake whenever we needed to slow down! Similarly, in

hedging also, we have to make effective use of the lever of the Amount apart

from that of the Rate.

Many a times I think the forex risk management practice resembles physical fitness. Everyone knows it is very important, but very few people do anything at all about it. Among those who hedge, few do it regularly, and fewer still do it scientifically.

The forex hedging landscape today is what the fitness industry scenario was 25-30 years ago, which is actually heartening. More people are aware of the need for physical fitness today than they were several years ago. Professionals keep sharing suggestions on diet, nutrition and fitness plans through newspaper articles. This encourages people to be more careful about their diet and to take up some sort of fitness regimen. Like people have become more health conscious over time, with more forex professionals writing about hedging, companies will certainly become more hedging conscious over time.

It was not always like

this

However, it was not like this some 25-30 years ago. Fitness

was equated with body building, which only wrestlers, boxers and some Hindi

movie villains spent time on. This is akin to people equating forex hedging

with only trading and speculation. Hindi movie heroes were generally not into

fitness at all (remember Rishi Kapoor’s paunchy look in the 1990s and Sanjeev

Kumar’s tyres in the 1980s?). Why, even cricketers were prone to muscle pulls

and injuries all the time due to lack of fitness.

Thankfully, the fitness movement is a real thing today. Not

only athletes and movie stars, but even corporate executives at all levels and

across age and gender are taking greater care of their bodies, following the

personal examples being set by corporate captains such as Rajiv Bajaj, Harsh

Mariwala, Anand Mahindra and many others. Some are even pursuing serious running,

cycling, some sports or the elusive six-pack abs, which is of the order of

running serious derivatives programmes in forex. The daily fitness walk is more

like basic hedging using Forward Contracts.

Today’s encouraging fitness landscape took a long time to

build, with years of hard work by the likes of Mickey Mehta, Milind Soman,

Rujuta Diwekar and several other fitness gurus, nutritionists, yoga veterans

such as BKS Iyengar and Baba Ramdev, and legions of unknown daily practitioners

who formed the bedrock of the fitness movement.

Coming to forex hedging, In its early days, post the 1991

Rupee devaluation and the introduction of LERMS in 1993, forex “hedging” was

mostly about trading in forex by large companies and diamond merchants, which

lasted till about 2000. Then came the Dollar-borrowing binge which ran from

2000 to 2008, during which companies threw all caution to winds egged on by

bonus hungry bankers, finally resulting in the massive derivatives disaster of

2008, after which forex hedging virtually became a bad word.

Through all this, pioneers like Mr. AV Rajwade, Mr. Jamal Mecklai, ourselves and many others have been talking about forex hedging for more than 25 years now. Reliable forex forecasting (with the 73% Reliability of Kshitij forecasts) and systematic, scientific hedging (the KSHITIJ Hedging Method ) came into being from 2006 onwards, helping companies deal with increased Rupee volatility. Slowly, very slowly, more and more companies are at least starting to listen to forex advisors more seriously. There is still a long way to go, but the outlook is encouraging.

Prevention, rather than

cure

The pursuit of fitness and well being is rooted in the maxim

of “Prevention is better than cure” and is entirely different from going to a

doctor in case of illness. People go to a doctor out of compulsion, usually

when a lot of damage is already done. At that time, the doctor’s medicines can,

at best, prevent the untoward and unfortunate, but cannot make the patient

healthy and fit. Similarly, taking a hedge at a time of extreme volatility, out

of compulsion, can at best prevent some forex losses, but cannot make the

company risk tolerant.

Just as, at its worst, lack of fitness can show up in

debilitating illness with ruinous costs, lack of forex hedging can cause severe

balance sheet damages. That is why, those who have understood the vital

importance of fitness pick up a fitness regimen out of choice and those who

view forex risk management as a vital part of business, take up the practice of

forex hedging on a regular basis, even if it is with simple forward contracts.

Benefits of FX Risk

Management

The first benefit of a well thought out hedging policy,

implemented properly, is that it makes a company more risk tolerant and enables

it to handle volatility much more calmly and with least damage. This is similar

to the increasing immunity levels through a regularly fitness regimen, which enables

us to ride over normal illnesses like the cold, cough and common flu with

relative ease.

Secondly, just as fitness reduces lethargy, makes us more

energetic and enhances our daily performance levels, a proper focus on forex

risk management brings greater efficiencies into a company’s day to day

functioning. How? The data and information flow, planning, focus on the future,

execution and the co-ordination and communication between various departments

of the company that is necessary for proper forex risk management, all together

add up to yield greater efficiencies.

It is easy to see that companies practicing proper forex

risk management are likely to be more efficient in their businesses, even

deriving a competitive advantage out of it, than those who either do not hedge

at all or hedge off and on or even haphazardly.

Never too late to start

Most people tend to give up on sports and fitness once they

start their working lives, largely due to lack of time. They take up fitness

again when they either find the luxury of time after their initial years of

struggle or they are hit by some illness or due to both reasons. Still,

whenever they start on fitness, it is never too late to start.

Similarly, most companies, especially SMEs who find

themselves dealing with issues of production, sales, garnering of finances and

scaling up, tend to neglect forex risk management due to lack of bandwidth.

They either start looking at forex when other parts of their operations have

stabilized or when they are adversely hit by volatility, or due to both.

By the same token, whenever a company starts to get serious

about forex hedging is good. It is never too late to start. The important thing

is to take up forex hedging seriously.

Very frankly, as forex advisors, the onus lies on us to win the respect of our clients. This piece of thought is for ourselves at Kshitij.com as well as for our peers in the forex advisory space.

Here is a common enough scenario across all forex advisors –

the advisor does a lot of studies, comes up with a forecast, devises a hedging

strategy and dishes it out to his client. The client takes it gingerly, makes a

herculean effort not to wrinkle his nose at it and then when he thinks the

advisor is not looking, quietly consigns the advice to the garbage bin near his

foot. And later, when the market moves in the manner predicted, it is the turn

of the advisor to make a herculean effort to avoid saying, “I told you so!”

Ever wondered why corporate hedgers tend not to heed the words of their forex advisors? Well, there is a reason for it, rooted in human psychology.

The thing is, all of us human beings – clients and advisors

alike, contrary to the assumption in economic theory, are emotional creatures

and not the emotionless rational beings we are assumed to be. We are less like

Mr Spock and more like Captain Kirk of Star Trek. This fact leads to many

unanticipated consequences, which need to be accepted as the normal, rather

than the abnormal. The whole new field of Behavioural Economics deals with

this, and it is here that we find the answer to why clients do not listen to

their forex advisors.

Dr Daniel Kahneman, the 2002 Economics Nobel laureate and

one of the leading lights of Behavioural Economics, in his seminal book

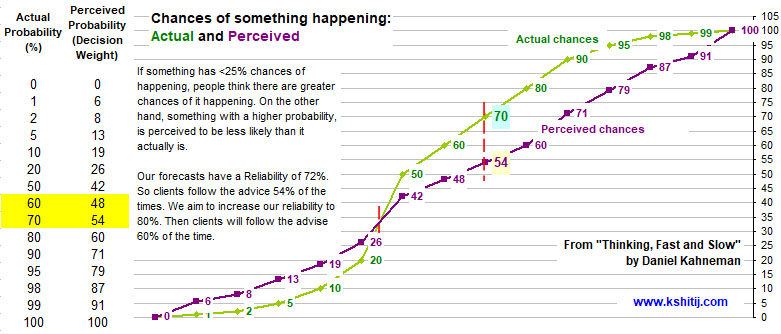

“Thinking Fast and Slow” has said that we human beings tend to overestimate the

chances of those things which in actuality have very low probability. For

instance, those things which have only a 1-2% statistical chance of occurring

are estimated has having 6-8% chance in the human brain. Conversely, we also

tend to underestimate the chances of those things which in actuality have very

high probability. For example, something with a 98-95% statistical probability

is humanly estimated as having a 87-79% chance of happening.

Why is this important to us and to this topic? It is seen that something which has a 60% statistical chance of occurring is underestimated by clients at 48% and something with a 70% chance is discounted to 54%. This means that if the suggestion of a forex advisor has 60% chance of being correct, in their minds, clients assume it to be 50%. And this is why they tend not to follow the advice as often as follow it. If the statistical chance of the advice being correct is 70%, it is discounted to 54% (a whopping 16 percentage points lower) in the client’s mind. It is at 70% Reliability that there is some hope that the clients may follow the advice a little more often. And, it is at 80% reliability that clients are likely to follow the advice 60% of the times! In other words, if forex advisors want clients to follow their advice most of the times, they need to exhibit a reliability of 80%.

It is not that corporate clients are a species from a

different planet. Is not common that all of us follow the doctors’ advice no more

than 50-60% of the times? Do we not discount the well meaning advice of our

friends? Why, husbands are notorious for not listening to their wives (who are

right even when they are wrong)! It is just the way the human brain is wired.

We tend to make larger than necessary concession for the chance that our

advisors may be wrong. In plain simple language, we don’t want to be caught on

the wrong foot because of our advisor’s mistake!

Furthermore, when the corporate client does not even know

the statistical track record of a forex advisor (other than experiential

anecdotal knowledge maybe), how is he expected to place any faith at all in the

advice? More ironically, when the forex advisor sanctimoniously says, “We are

not in the business of forecasting currency movements, we are in the business

of managing risk”, where does that leave the hapless importer/ exporter? He

jolly well needs to know where the market is going, because how do you

determine risk without having an idea of where the market is going, dammit!

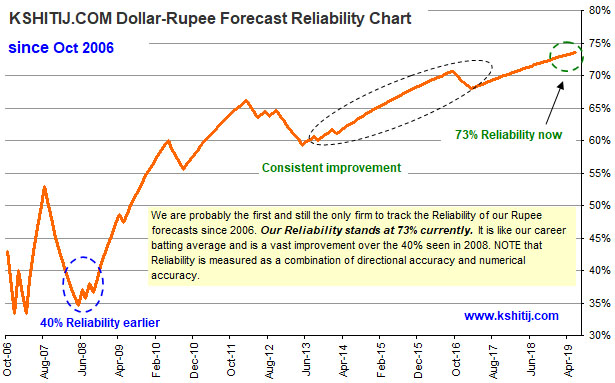

We, at Kshitij.com started publishing a track record of the reliability of our Dollar-Rupee forecasts in 2006. We were probably the first and are probably still the only ones to do so. Since there was no model available, we devised our own criteria. As per that, our Dollar-Rupee forecasts have a 78% reliability over the last 13 years. That is like a career batting average. But, we found the criteria to be a little loose and relaxed. So we tightened the criteria. As per this second (and tighter) set of criteria, we currently have a 72% reliability. However, not satisfied with that either, we have now tightened the criteria even further and we find we stand at 60% reliability. Talk about making life difficult for ourselves!

Now, here’s another very important fact about human

psychology. Human beings might be irrational, they might be emotional. But, in

the end people are not unreasonable and they do have a heart. Clients do

ultimately appreciate honest, undying effort. In this, we are happy to share

that over time, slowly, as our forecasts have improved, our clients

are listening more to us. And are thus benefiting more.

Performance measurement can be a huge “let us take it to the next level” movement for the forex advisory practice, because, ultimately, let’s face it, the onus lies on us.

The currency market witnessed two main trends in 1999 – the Euro’s decline and the rise of the Yen. These trends coalesce into a 21.5% decline in Euro-Yen, from 132 in the beginning of the year to 102 in December. In the last quarter of the year, the market witnessed a very strong correlation between the strength of the US Equity market and the strength of the US Dollar a gainst the Euro. The common refrain in the currency market was, “The Dow leads the Euro pip-by-pip.” In this paper we examine the relationship between the Dow Jones Industrial Average and the Dollar-Euro rate (EURUSD inverted) more closely.

Dow-Dollar are highly correlated

As can be seen in the Chart above, the DJIA and the Dollar have moved largely in tandem after 1995. The period 1994 to 1999 itself displays a high correlation on 78.9%, but this can be broken into 2 periods, as seen in the table alongside (detailed table provided at the end). From this we draw an obvious conclusion – the Dollar strengthens along with the Dow.

Vulnerability

There is a flip side to this observation – When the Dow is not rising, the Dollar falls. In fact, the Dollar tends to fall more (in relation to its own range) than the Dow in such periods.

Observe the periods Aug-Oct ’97, May-Aug ’98 and July-Oct ’99. In these periods, each lasting 3-4 months, the Dow fell an average of 14% (6.8% of its entire 1994-199 range) and correspondingly the Dollar fell an average of 7%. (64.42% of its entire 1994-199 range). Even the period Jan ’94 to March’95 exhibits the same features – the Dow rose very slowly, accompanied by a prominent downtrend in the Dollar.

The Dollar is disproportionately vulnerable to weakness in the Dow.

Polynomial Curves

We have plotted Polynomial curves of the 6th degree for both markets. Their projected values 60 trading days hence can be seen on the graph above.

According to these projections, the Dow should continue to rise (but with lesser momentum than seen till now) to reach a little higher than 11500. This is in keeping with our earlier analysis (see “The Colour of Money” dated 21/12/1999) wherein we have contended that the Dow should not see a sustained rise beyond 11600 over the next 2-3 months.

The curve for the Dollar-Euro rate indicates a sharp increase in the Dollar’s strength, taking the rate to 1.10 (or the Euro-Dollar rate to 0.9090). We are inclined to take this projection with a pinch of salt. Here is why:

the polynomial has never risen so sharply (as projected) in the period considered. The natural question is, can it now rise exponentially?

If the Dow is not expected to rise very sharply, then it should not be possible for the Dollar to rise sharply either. As such, once again the projection is suspect.

And if the actual market does turn out to obey the polynomial’s projection, the Dollar’s strength can be expected to be capped near 1.10 (or 0.9090 on the Euro-Dollar rate).

Conclusion – Careful on the Dollar, please

If, for any reason (fundamental and or technical), you happen to view the bullishness for the US economy (read Nasdaq / Dow) and the US Dollar with caution or dread, this piece should give you another reason to add to your list of worries.

There would have to be some sea-change, something totally unexpected, something not yet priced into the market, something which is exceptionally favourable to the USA for the Dow and the Dollar to continue to soar.

Apart from all of the above, in the markets, they say, it pays to Buy Low and Sell High.

Study reviewed on 2 Jul, ’01

Recap We had last studied the relationship between the Down Jones Industrial Average and the $-Euro (inverse of Euro-$) rate on 28th December ’99, and had detected a strong positive correlation between the two. This correlation suggested that the Dollar would weaken against the Euro due an expected fall in the DJIA Index.

Ironically, soon after we completed the study, the market proceeded to prove its findings to be incorrect. Over the period 30th Dec to 14th March, while the Dow fell from 11497.12 to 9811.24, the Dollar actually strengthened against the Euro as the Euro-$ rate fell from 1.0088 to 0.9680. In fact the Dollar continued to strengthen against the Euro right through to May when the Euro hit an all-time low of 0.8845.

Inversion We thought it would now be a good idea to re-examine this relationship. The graph alongside strongly suggests that the positive correlation seen uptil Dec ’99 has been broken and that in the months ahead the Dollar can continue to gain against the Euro even as the DJIA Index falls. The thick Orange and Green “Trend Curves” are Polynomial curves generated by the statistical Method of Least Squares and have traced the overall direction and movement of the two series (Dow and Dollar) till now. Since these can be used to predict the future movement of the underlying series and these two curves are seen to be crossing each other now, we are forced to seriously consider the possibility that the Dollar can now continue to rise even as the DJIA falls.

Rationale What could, however, bring about such a change in the relationship, a change which seems to fly in the face of economic logic (how can a country’s currency strengthen over a long period of time while its stock market falls?)

1) The best explaination that we can find is that a strong Dollar (against the Euro) continues to be in the best interests of the USA, which continues to be dependent on foreign investments to fund its massive trade deficit. The Dollar is the symbol of US supremacy and the USA will do everything within its means (and more) to safeguard it. 2) The Dollar is an international issue, while the DJIA is more of a domestic issue. The US can afford to let the Dow lose ground as long as the Dollar remains strong. 3) If the Dollar weakens along with a weakening of the Dow, the foreign investor will suffer on account of both a fall in the Dow as well as currency depreciation. Surely a strengthening Dollar has been a big incentive drawing investors to the USA. It is in the interest of the USA to see that this incentive remains intact. 4) Oil prices, now ruling near $30-31 per barrel are unlikely to go up much further from here and thus, going forward, they may not add significantly to inflation. On the other hand, if the Dollar weakens at this juncture, the trade gap will increase much more. 5) The Oscillators on the Daily and Weekly chart support a bearish Euro view. 6) If a currency is to be manipulated, the US can be expected to do a much better job than the hamhanded ECB.

So continues the battle of the Dollar versus the Euro, for it is a battle to own the rights to the universal symbol of Wealth – will Wealth be symbolised by the $ or by an “E”.

Study reviewed on 6th Feb, ’01

We last studied the relationship between the Dow Jones Industrial Average and the Dollar-Euro rate(inverse of the conventional Euro-Dollar rate) on 28th Dec. ’99 and on 2nd July 2000.

The conclusions so far have been that: (a) The Dow and the Dollar are positively correlated (the Dollar strengthens alongwith the DJIA) and that (b) The Dollar can strengthen even if the Dow does not.

The second conclusion comes in for greater scrutiny in this Research.

The clue that it is not only the Dow that drives the Dollar-Euro rate comes from the fact that the Dollar strengthened over 1999-2000 even though the Dow remained largely rangebound between the two extremes of 11700 and 9800 (Period C alongside). Further, in the period Jan-March 2000, the Dollar strengthened even while the Dow fell and then later, over the period Oct-00 to Jan-01, USD fell while the Dow was steady.

We can say that during these two periods, the Dollar was following the NASDAQ rather than the Dow, with Correlation between the Nasdaq and Dollar-Euro during these periods being in the region of 55-77%(as shown in the Correlation Table above).

Thus, we now need to consider the future of not only the Dow Jones, but also of the Nasdaq to be able to forecast movements in Dollar-Euro (or more conventionally, Euro-Dollar).

Over the last few years the importance of the US Equity markets as a recipient of foreign capital inflows, especially from Europe, has grown considerably. While forecasting the long-term Dollar-Deutschemark rate used to be a matter of forecasting the 10 Year US Bond – German Bund interest rate differential till a few years ago, it is now probably more useful to try and predict the movements in the Dow Jones and the Nasdaq.

Looking ahead, while the Dow Jones stays above 10300, and certainly above 9700, the chances of it climbing above 11000 again remain alive. If the recent Interest Rate cuts in USA and the proposed Tax cuts fail to deliver the goods, only then would the Dow fall below 10300. As of now it might be a little early to write off the Dow.

It has been a very long time since Fiscal Policy was used as a tool in Economy management. It is also much more difficult to track and analyse the effects of Fiscal Policy and as Alan Greenspan’s Monetary Policy has held sway over the past decade, the markets are probably not factoring in the Tax Cuts proposed by President Bush well enough. The possibility that these Tax Cuts may prove to be a positive catalyst for US Stocks has to be borne in mind.

Forecasting for the Nasdaq is tantamount to taking a stance on the future of “Technology”. The bottom line, signified by the very strong Support at 2000-1700, is that Technological (and IT) advancement cannot be reversed. At the same time, we are not going to see the logic-defying valuations of early 2000. Unless there is indeed a “Hard Landing”, it would not be inconceivable for the Nasdaq to rise to 3400 by the end of the year, as compared to 2627 on 12th January 2001.

The first and obvious implication is that taking a stance on Dollar-Euro (or Euro-Dollar) is almost the same as taking a stance on the US Equity markets. Thus, a Long-Dollar / Short Euro position can be hedged with Put Options on the DJIA and on the Nasdaq. Or, looking at it the other way round,investments in US Equities can be hedged with a Short-Dollar / Long Euro position or with a Euro Call Option.

In our last report (27-Feb-26, UST10Yr 4.01%), which was published just one day before the start of the US-Israel-Iran War on 28-Feb, we had continued to target 4.60% on the US10Yr based on expectations of higher Crude. At that time, we were looking for Brent to rise …. Read More

WHAT'S NEW?

Apr’26 Crude Oil Report

The escalation of war between US and Iran throughout March-26 has led to a rally in Brent prices to as high as $119.50, exceeding our bullish targets by a large margin, much ahead of expected time. Will it remain bullish for the coming years?… Read More

WHAT'S NEW?

Mar’26 EURUSD Report

Our view of a fall towards 1.14 seems to be playing out well so far as the tensions in the Middle East and the US-Iran conflict have triggered a rise in Dollar Index and crude oil prices, thereby weakening to Euro to 1.1507 so far in Mar-26. Will it again attempt to rise targeting 1.20? Or will it remain below 1.19/20 now and see an eventual decline to 1.10? …. Read More

WHAT'S NEW?

Apr’26 GOI Report

In our 09-Mar-26 report (10Yr GOI 6.69%) we had warned that the sharp rise in crude due to the US-Iran conflict could push Brent toward $134, which would lift CPI toward ~6.2%, eliminating any chance of RBI easing, and potentially force tightening. This inflation shock, along with higher US yields, was expected to push the 10Yr GOI up to … Read More

WHAT'S NEW?

Jan’26 USDJPY Report

In our 10-Dec-25 report (USDJPY 156.70), we expected the USDJPY to trade within 154-158 region till Jan’26 before eventually rising in the long run. In line with our view, the pair limited the downside to … Read More