Dollar-Rupee at 60? Or 172?

Jan, 25, 2020 By Vikram Murarka 0 comments

NOTE 1: This is not a strictly predictive report. This is more of an exploration of possible multi-decade trends for Dollar-Rupee. It aims to lay out two main possibilities (of either Rupee strength towards 60 against the US Dollar, or weakness towards 172) before policy makers; and to suggest that we, as a country, should choose the path of Rupee strength.

NOTE 2: As per our analysis in Chart 6a and Chart 6b herein, the post-Independence rise in USD-INR might have already gotten over at 74.4825 in Oct-2018. The validity of this analysis hinges on the acceptance of a particular rare phenomenon. We are accepting this rare phenomenon because

(A) acceptance thereof allows the Rupee movement since 2008 to fit in with some other movements in the global currency market and (B) although rare, the phenomenon cannot be rejected (a bit like, although rare, a white peacock is accepted as a peacock, not rejected.)

NOTE 3: We are sharing this analysis because (A) we sincerely believe it has merit and (B) there is a very important policy implication to be considered at the highest level (please refer Note 1 above).

NOTE 4: There is a 30-50% chance that our analysis is wrong. But, there is also a 50-70% chance that the analysis is right. Even if the analysis is wrong and USDINR has not already seen a top at 74.4825 in Oct-2018, there is a very good chance (near 70%) that the post-Independence weakness of the Rupee can naturally come to an end anywhere between 75-77. That is, if the economic orthodoxy of the authorities does not stand in the way and disrupt the natural movement of the USDINR. The alternative would be to see Rupee weakness continue into perpetuity.

You may also like:

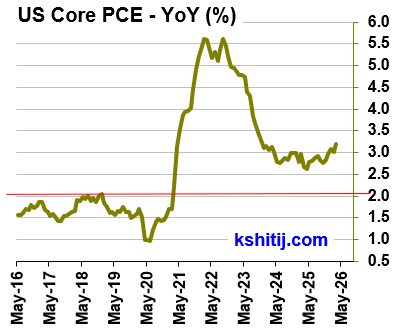

In our last report (29-Apr-26, UST10Yr 4.35%), we had said that the FED was likely to leave rates unchanged, which it did. We had also said that “once Kevin Warsh comes in, the FED is more likely to cut, responding to …. Read More

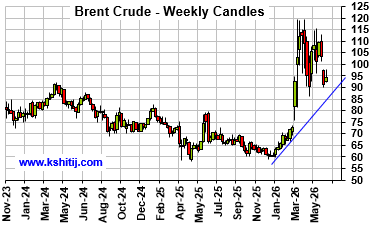

In our May 2026 report (4-May-26, Brent @ $110.75), we expected Brent to test $90.50 by Jul-26, followed by a rise to $145.13 by Sep-26 and $161.93 by Dec-26. Sustained trade below $100 was expected to be seen only on a credible resolution of the US-Iran war, which looked unlikely … Read More

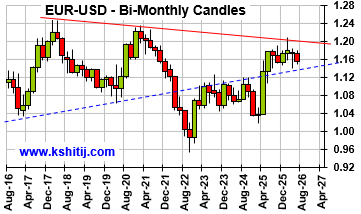

In our May 2026 report (11-May-26, EURUSD 1.1762), we expected the Euro to rise to 1.1950 by May-26 before falling towards 1.16-1.14 in the coming months. We delayed the fall to 1.10 from the earlier expected Aug-26 to Mar-27 as the Dollar Index remained within a broad range for more than expected …. Read More

In our 11-Apr-26 report (10Yr GOI 7.03%) we had retained our bullish view on Brent towards $134 by Sep-26, while allowing for a near term dip to $95 on hopes of a US-Iran resolution. Brent fell to $89.93, lower than … Read More

In our 10-Dec-25 report (USDJPY 156.70), we expected the USDJPY to trade within 154-158 region till Jan’26 before eventually rising in the long run. In line with our view, the pair limited the downside to … Read More

Our June ’26 Dollar Rupee Monthly Forecast is now available. To order a PAID copy, please click here and take a trial of our service.