Series on Forex Hedging - Cash In On Cash-Spot

Jun, 25, 2012 By Vikram Murarka 0 comments

Cash-Spot is one of the lesser known technical concepts in the forex market. Nothing earth shattering, really, but it is always good to know the technical details of the market we operate in. The forex rates that we see in the normal course, quoted on the screens, in forecasts or in the papers, are all Spot rates (unless specifically mentioned otherwise) and do not pertain to today. Strange? To explain a little clearly, we introduce a few definitions, alongwith examples.

| CASH-SPOT: DEFINITIONS AND EXAMPLES | ||

| Term | Definition | Example |

| Cash date or Trade date | The date of the transaction, say “today” | If today is 25-June-12, then Cash date is 25-June-12 |

| Spot date | Second working day from the Cash date, or day after tomorrow | 27-Jun-12 |

| Tom date | Tom is short for “tomorrow” and is the next working day from the Cash date | 26-Jun-12 |

| Spot Rate | The rate quoted and transacted today for settlement (debit/ credit) on the Spot date | Say, the rate is 55.95. This is the rate we normally see, hear and talk about. |

| Cash Rate | The rate applicable for settlement (debit/ credit) today itself, on the Cash date | This is usually lower than the Spot Rate. Since the Spot Rate is 55.95, the Cash Rate may be 55.93. The difference between the two rates is known as the Cash-Spot rate or Cash-Spot difference. |

| Tom Rate | The rate quoted and transacted today for settlement (debit/ credit) tomorrow, on the Tom date | This is lower than the Spot Rate, but higher than the Cash Rate. Since the Spot Rate is 55.95, the Tom Rate may be 55.94. |

In simpler terms: Spot Date = Trade Date + 2 working days. Cash Rate = Spot Rate minus Cash-Spot Difference.

Depends on Interest Rates

In the case of Dollar-Rupee, the Cash Rate is usually lower than the Spot Rate in the same way that the Spot Rate is usually lower than a Forward Rate. In other words, compared to the Spot Rate, the Cash rate is usually at a Discount, whereas the Forward rate is usually at a Premium. Note: any date after the Spot date is a Forward date.

The Cash-Spot market is largely a high-volume interbank market as it is based upon banks borrowing in one currency and lending in the other, usually to meet overnight reserve requirements. Thus, the Cash-Spot Difference depends on the difference between the Overnight or Call rates between the two currencies concerned.

If there is a holiday, or a couple of holidays (as over the weekend) between the Cash and Spot dates, then also the T+2 definition applies. In such case the Cash-Spot difference understandably increases.

Market Timings

The Cash-Spot market usually operates between 9.00 AM and 11.30 AM, with some stray deals being done till 12.00 Noon.

Is the Cash-Spot quoted?

Yes, the Cash-Spot and Cash-Tom rates are quoted on most forex rate services such as Reuters, Bloomberg, Newswire 18 and Tickerplant. We also report it daily in the Forward Rate Sheet that is sent out by e-mail to the subscribers of our daily Rupee Update service.

What does it mean for Exporters?

When an Exporter sells Dollars to a bank at the Spot Rate (say 55.95), he should get a credit into his Rupee account on the Spot date. If he insists on a credit on the transaction date (Cash date), the bank may well deduct the Cash-Spot difference (say 2 paise) and credit his account at the Cash rate, say 55.93. So, as a general rule, an Exporter should not insist on a same day credit.

What does it mean for Importers?

When an Importer buys Dollars from a bank at the Spot Rate, his Rupee account ought to be debited on the Spot date, and not on the transaction date. This is something that the Importer should be careful about and check on a regular basis. On the other hand, it may be good for the Importer to pay for the Dollars at the Cash rate as it would be cheaper than the Spot rate. In such case a debit on the transaction date would be justified.

You may also like:

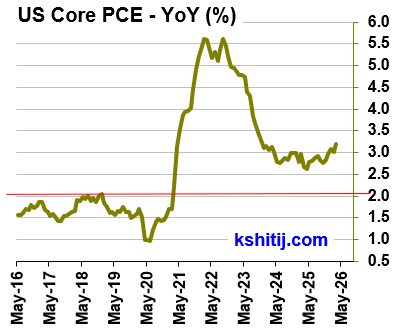

In our last report (29-Apr-26, UST10Yr 4.35%), we had said that the FED was likely to leave rates unchanged, which it did. We had also said that “once Kevin Warsh comes in, the FED is more likely to cut, responding to …. Read More

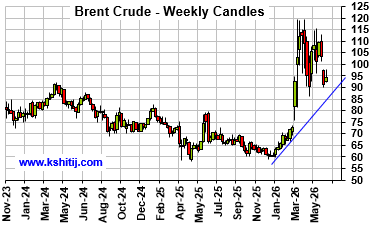

In our May 2026 report (4-May-26, Brent @ $110.75), we expected Brent to test $90.50 by Jul-26, followed by a rise to $145.13 by Sep-26 and $161.93 by Dec-26. Sustained trade below $100 was expected to be seen only on a credible resolution of the US-Iran war, which looked unlikely … Read More

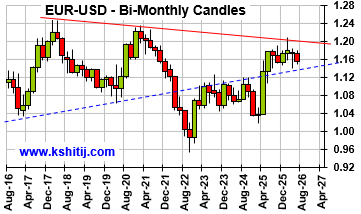

In our May 2026 report (11-May-26, EURUSD 1.1762), we expected the Euro to rise to 1.1950 by May-26 before falling towards 1.16-1.14 in the coming months. We delayed the fall to 1.10 from the earlier expected Aug-26 to Mar-27 as the Dollar Index remained within a broad range for more than expected …. Read More

In our 11-Apr-26 report (10Yr GOI 7.03%) we had retained our bullish view on Brent towards $134 by Sep-26, while allowing for a near term dip to $95 on hopes of a US-Iran resolution. Brent fell to $89.93, lower than … Read More

In our 10-Dec-25 report (USDJPY 156.70), we expected the USDJPY to trade within 154-158 region till Jan’26 before eventually rising in the long run. In line with our view, the pair limited the downside to … Read More

Our June ’26 Dollar Rupee Monthly Forecast is now available. To order a PAID copy, please click here and take a trial of our service.