The Forward Rate is not a Forecast

May, 14, 2012 By Vikram Murarka 0 comments

This might be a little basic for old hands in the market, but there is often a misconception among new entrants that the Forward Rate is a forecast of where the rate is going. For instance, if on 09-May the Dollar-Rupee Spot rate is 52.82 and the Forward Rate for 30-June is 54.39, many people think that market is expected to be at 54.39 on 30-June. This is not the correct interpretation.

This might be a little basic for old hands in the market, but there is often a misconception among new entrants that the Forward Rate is a forecast of where the rate is going. For instance, if on 09-May the Dollar-Rupee Spot rate is 52.82 and the Forward Rate for 30-June is 54.39, many people think that market is expected to be at 54.39 on 30-June. This is not the correct interpretation.

Function Of Interest Rate Differentials

In the forex market, the Forward Rate is not a forecast. It is simply the rate at which the market is ready to transact today, for a future date. Therefore, 54.39 is the rate at which the market is willing, on 09-May, to transact for value date 30-June. That’s it. The actual rate on 30-June is quite likely to be either much higher (maybe 55.30) or much lower (maybe 52.00) than 54.39. Yes, this does not seem to make sense. Why should the market transact at 54.39 for 30-June if the rate is not expected to be at or near 54.39 on 30-June? How can the banks (the dominant players in the forex market) risk a loss? The fact is that the banks are not taking a view on the future exchange rate when transacting a Forward Rate. They are really lending one currency and borrowing another currency for the same stated value date (or maturity date) and the Forward Rate is calculated so as to bridge the interest rate differential between the two currencies. Thus, neither of the banks on either side of the trade stands to make a loss from an interest rate perspective. This is how the forex forward rate came into being and is arrived at even today. The forward rate is simply a function of the interest rate differential between two currencies. It is not the expected future exchange rate.

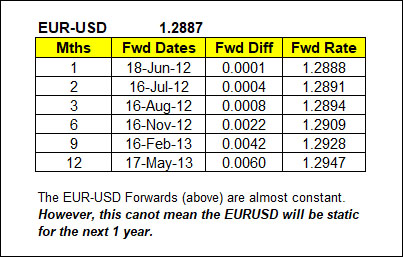

Here's Proof

Hard to believe? OK, here’s proof. The interest rates in USA and Europe being very low, the interest rate differential between the USD and the EUR is negligible. As such, the forward rate for the EURUSD is almost the same as the spot rate. For instance, on 14-May, the 3-mth USD Libor is 0.47% while the 3-mth EUR Libor is 0.62%. Thus, the interest rate differential is 0.15% and the 3-mth EURUSD forward rate is 1.2894, which is almost the same as the spot rate of 1.2887. If the forward rate were the forecast of where the market is going to be in the future, the implication of the above paragraph would be that the EUR-USD rate should not go anywhere for the next three months; or in other words, the rate is going to be same three months hence. However, we know that this is not possible. The Euro has at least a 66.7% chance of moving around (whether up or down) rather than remaining static. Therefore, whatever else it may be, the forward rate is not a forecast for the future. The above is especially true of forward exchange rates among countries which have allowed free flow of capital between themselves, or countries with full capital account convertibility. Even in India, which has limited capital account convertibility, the interest rate differential between USA and India now influences the short-term forward rate to a large degree, especially given the fact that progressively larger amounts of debt inflows are being allowed into the country which the foreign investors are allowed to hedge in the domestic forex market.

Market Moves Different From Forwards

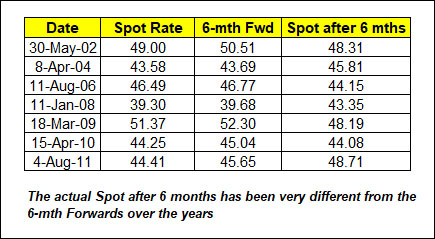

In India, the forward US Dollar is usually quoted at a premium to the Rupee, or, the Forward Rate is higher than the Spot rate. If the forward rate were to be a relatively accurate forecast of future Spot, then the Rupee ought to have depreciated against the Dollar all the time, it should never have appreciated. However, we have seen episodes of significant Rupee appreciation - from 49 to 39 (2002-2008), from 52.18 to 43.85 (2009 to 2011) and from 54.30 to 48.60 (2011 to 2012). Yes, the Futures in other markets such as commodities, interest rates and equities, could be taken as the prevailing market consensus about where the market rates will end up in the future, but not so in the forex market. This is a peculiarity of the forex market. Most people who enter the forex market harbour this misconception initially, but it is thankfully corrected pretty soon. So, next time you want to know where Dollar-Rupee is going to be in the future, don’t rely on the Forward. Look for a professional forecast!

You may also like:

For the last few months we have been looking for Crude to rise towards $130-190 and pull up the US CPI towards 4.6% and the US10Yr Yield to 5.4% by Jan-27. This view has clearly gone wrong with Brent falling sharply below $90 as a result of the US-Iran peace deal, which is the …. Read More

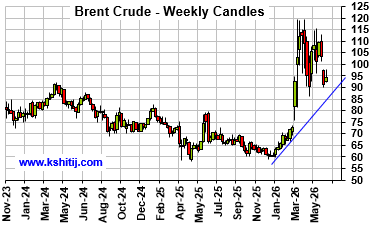

In our May 2026 report (4-May-26, Brent @ $110.75), we expected Brent to test $90.50 by Jul-26, followed by a rise to $145.13 by Sep-26 and $161.93 by Dec-26. Sustained trade below $100 was expected to be seen only on a credible resolution of the US-Iran war, which looked unlikely … Read More

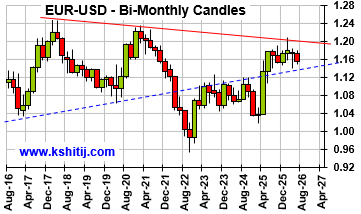

In our May 2026 report (11-May-26, EURUSD 1.1762), we expected the Euro to rise to 1.1950 by May-26 before falling towards 1.16-1.14 in the coming months. We delayed the fall to 1.10 from the earlier expected Aug-26 to Mar-27 as the Dollar Index remained within a broad range for more than expected …. Read More

In our 11-Apr-26 report (10Yr GOI 7.03%) we had retained our bullish view on Brent towards $134 by Sep-26, while allowing for a near term dip to $95 on hopes of a US-Iran resolution. Brent fell to $89.93, lower than … Read More

In our 10-Dec-25 report (USDJPY 156.70), we expected the USDJPY to trade within 154-158 region till Jan’26 before eventually rising in the long run. In line with our view, the pair limited the downside to … Read More

Our June ’26 Dollar Rupee Monthly Forecast is now available. To order a PAID copy, please click here and take a trial of our service.