Global Equities: Why we are unable to buy

Oct, 26, 2017 By Vikram Murarka 0 comments

26-Oct-17

Dow 23329/ Sensex 33056

RECAP

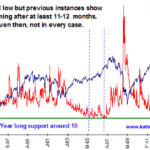

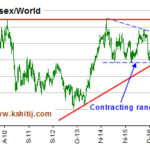

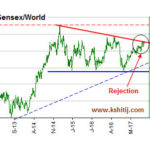

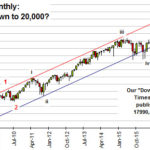

Our apologies that we were unable to publish this report in October 2017. In our last report dated 04-Sep-17, we said, “We remain cautious on the Dow and Sensex and bullish on the Shanghai, which is likely to outperform both.” We have been surprised by the continued strength in Dow Jones (23329) which has broken well above 22500 instead of starting a decline towards 20000. The Sensex (33056) has also moved up from 31809 instead of falling towards 30000. Thankfully, our bullishness on the Shanghai paid off a bit, although it could not compensate for our bearishness on the Dow and on the Sensex.

EXECUTIVE SUMMARY

While we have been surprised by the continued bullishness in global Equities in the last couple of months, we still see limited upside over the next month or two and still see chances of a corrective fall thereafter.

To read the full report.......... DOWNLOAD

You may also like:

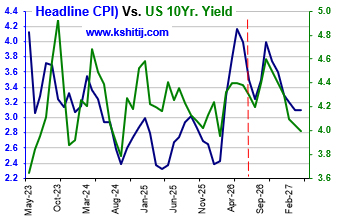

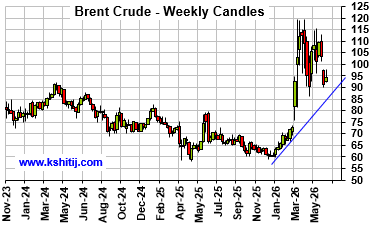

For the last few months we have been looking for Crude to rise towards $130-190 and pull up the US CPI towards 4.6% and the US10Yr Yield to 5.4% by Jan-27. This view has clearly gone wrong with Brent falling sharply below $90 as a result of the US-Iran peace deal, which is the …. Read More

In our May 2026 report (4-May-26, Brent @ $110.75), we expected Brent to test $90.50 by Jul-26, followed by a rise to $145.13 by Sep-26 and $161.93 by Dec-26. Sustained trade below $100 was expected to be seen only on a credible resolution of the US-Iran war, which looked unlikely … Read More

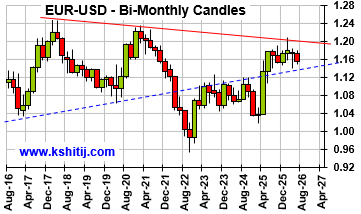

In our May 2026 report (11-May-26, EURUSD 1.1762), we expected the Euro to rise to 1.1950 by May-26 before falling towards 1.16-1.14 in the coming months. We delayed the fall to 1.10 from the earlier expected Aug-26 to Mar-27 as the Dollar Index remained within a broad range for more than expected …. Read More

In our 11-Apr-26 report (10Yr GOI 7.03%) we had retained our bullish view on Brent towards $134 by Sep-26, while allowing for a near term dip to $95 on hopes of a US-Iran resolution. Brent fell to $89.93, lower than … Read More

In our 10-Dec-25 report (USDJPY 156.70), we expected the USDJPY to trade within 154-158 region till Jan’26 before eventually rising in the long run. In line with our view, the pair limited the downside to … Read More

Our June ’26 Dollar Rupee Monthly Forecast is now available. To order a PAID copy, please click here and take a trial of our service.