Why Forex volatility is increasing and how to tackle that

Jun, 29, 2009 By Vikram Murarka 0 comments

Rupee Volatility has increased The last couple of years have been particularly painful for Corporate India in many ways. Forex Risk Management has been one of the ways by which several hundred crores were lost. In one famous case, a company lost close to Rs 1500 Crores, and went from a net profit in 2007-08 to net loss in 2008-09. Also famously, an Accounting Standard was changed to allow companies to capitalise forex losses on foreign loans.

What went wrong? Most obviously, there was a sharp rise in Dollar-Rupee volatility. Compared with an annual range of 10% (between 43 and 47) from 2003 to 2007, Rupee gained 11% in 2007 and fell 33% in 2008-09.

The less obvious, but more important, thing that went wrong was that the forex risk management techniques used by Corporates came a cropper.

This article makes two contentions. Firstly, forex volatility is here to stay and the sooner Corporate India learns to deal with it, the better. Secondly, extant forex risk management techniques of Corporate India are by and large illequipped to deal with volatility (as has been amply demonstrated) because of some fundamental flaws. The article does not end on a negative note, though. It proposes a set of questions that the top management, including the Board, of companies needs to introspect on and answer, if they want to be able to deal with the new reality of forex volatility.

Volatility to remain high

Over the years, there has been a trend increase in Dollar-Rupee volatility, measured by the percentage movement in a month. The Rupee used to fluctuate an average of 1% (or 45 paise) earlier, but the monthly fluctuation is now averaging 5% (about 225-250 paise). Moreover, the volatility is likely to remain above 3% (135-150 paise) in the future.

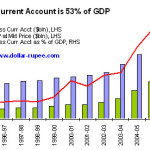

The main reason behind the structural increase in volatility is the growth of India's Current Account, including exports and imports of both goods and services, and India's Capital Account, which is witness to a high degree of volatility in portfolio investment flows. This has led to a huge increase in the daily turnover in the Dollar-Rupee market, to such an extent that it is now increasingly difficult for the RBI to contain the volatility on a daily basis. As the economy continues to grow and open up, it is unlikely that forex volatility is going to decrease. As such, the sooner Corporate India realizes that forex volatility is a fact of life and learns how to deal with it, the better.

Unfortunately, the way Corporate India has been managing forex risk so far is woefully inadequate to deal with currency volatility. The bleeding financial statements of companies are a testimony to this fact

Fundamental Flaws

The forex risk management systems in Corporate India suffer from some fundamental flaws. Three of these flaws are listed below :

1. No Benchmark

The unadmitted, but implicit, objective of forex risk management in a very large number of companies is to try and beat the market. There is a lot of pressure on the forex desks in companies to make profits. Do not go by what companies say in their annual reports. Ask the dealers and risk managers in the treasury departments of companies to verify this statement.

This happens because a most companies set no Benchmark by which forex risk management is to be guided. As a result, the market becomes the default benchmark and everybody tries to beat it. Hedging decisions are assessed on whether or not the hedge beats the market.

2. Fixed Benchmark, if at all

The few companies that work with Benchmarks tend to have a Fixed Benchmark for the whole year. One particular USD-INR rate is decided upon during the annual budgeting exercise in February-March, and then hedges are undertaken accordingly. This is done because (a) a fixed benchmark lends itself easily to budgeting (b) the marketing and production departments in a company do not want to deal with a "non-domain" variable and (c) there is still an innate "wish" in the minds of most people that exchange rates should remain steady.

<p>However, this approach is far removed from reality. The currency market, like most other markets, is volatile and given to wild swings. The factors on which the annual currency forecast (and benchmark) is based are likely to change. As such, there is a need to revise the Benchmark. Unfortunately, the system is inflexible and does not allow for changes in benchmarks, does not allow for any course correction.

3. No Budget for Hedging

It would be a very rare company, indeed, that had set aside a budget for Hedging in 2007 and 2008. Although every activity in business has a budget allotted to it, be it as mundane as the daily upkeep of toilets, Forex Hedging is supposed to be, or so it seems, costless. That is why forex hedging budgets are unheard of. And that is why we witnessed the phenomenon of hordes of companies taking on 1x2 Put Risk Reversals in 2006 and 2008 to hedge their Exports.

Buying a simple, plain vanilla Put costs money and no company had provided for that. So everybody tried to go in for "zero cost options" and ended up with losses that were several times higher than the option premium they could have chosen to pay earlier on plain vanilla Puts.

Nine Vital Questions

Of course, it is easy to point out what's wrong. It is more difficult to suggest a solution. Companies need to do some hard introspection if they want to find a way out of the current mess that is forex risk management. A set of nine vital questions is proposed below, which companies can ask themselves. The answers to these questions can pave the way for better forex risk management going forward.

QS 1. What is our FX Risk Management Agenda?

The agenda could include anything, ranging from "We want to avoid losses" to "We want to make profits" to "We want to train our people" to "We want to upgrade our treasury software" etc.

Here, let it be explicitly added, there is nothing wrong in having "We want to make profits" as the agenda of forex risk management. What is important is that the objective be approached in a proper manner.

QS 2. Have we quantified our FX Risk Management Objectives for the year?

Whatever objectives have been included in the Agenda in (1) above, they need to quantified. For instance, if the agenda is to "Avoid losses", it needs to be quantified as to losses beyond which level are to be avoided, because losses cannot be totally nullified without sacrificing profitability. This also presupposes that work has been done to estimate what quantum of losses is possible and what impact it can have on the companies financials.

Similarly, if the objective is to make profits, the company needs to estimate the profit potential and needs to set out the profit targets that need to be achieved. It also needs to quantify the potential risk in its pursuit of profits.

Without putting numbers to the objectives, the objectives will remain mere homilies.

QS 3. The production and marketing guys have their budgets. Have we worked out a Hedging Cost Budget?

Any and every activity requires some expenditure. Then why not Hedging? Stop Losses on Forward Contracts that go wrong and Option Premium on plain vanilla puts and calls would be paid for from the Hedging Cost Budget. It would make the life of the forex risk manager much easier and actually enable him and empower him to achieve the set objectives.

QS 4. How do we measure FX Risk Management performance? Are we trying to beat the market, or better a Benchmark?

In the absence of quantification of objectives, it becomes difficult to assess the performance of the FX Risk Management function. And by default, and by application of accounting rules, the company ends up trying to beat the market. This happens despite knowing that it is impossible (and even unadvisable) to try and beat the market on an ongoing basis.

QS 5. Is our Benchmark based on the past, present or future?

In the rare instance where a company (say an Exporter) sets a Benchmark, it tends to take the rate on the date of bill of lading as the Benchmark. Or sometimes the average exchange over the last 3 to 6 months may be taken as the Benchmark. Another common practice is to take the Forward Rate on a particular date as the Benchmark. The question is, are these practices effective and correct? If not, is there a better way?

QS 6. Where does Risk lie: in the past, present or future?

This is a rhetoric question. A moment's thought will tell us that risk lies neither in the past not the present, but in the future. And we also know that the future is likely to be different from the past and the present. So, it is the future that the FX Risk Management team should be concerned about.

QS 7. The market is ever changing. Is our benchmark fixed? Or Dynamic?

In anticipating the future, companies tend to make a "single number" forecast for the entire year ahead and take that to be the benchmark. The reasons why they do that have been outlined earlier in the article. But, it is hardly correct to do so, because the conditions on which that forecast was made are quite likely to change in the future. As such, there will be a need to revise the forecast based on the new, changed conditions. How many companies allow for such change in forecasts and Benchmarks?

QS 8. Are we more concerned with the performance of our Hedges than of our Exposures? Why?

Most companies become very concerned when a Hedge (Forward Contract or Option) goes out of money. In a case where the Exposure (the Export or Import itself) is not fully hedged (an optimal hedge ratio would be about 54%), there should actually be joy if a Hedge goes out of money because when a Hedge goes out of money, the Exposure ends up making money.

The problem occurs because within companies, the profit or loss on Hedges is deemed to be "Treasury profit/ loss" while gains/ losses on the Export/ Import itself are taken to be non-treasury, business gains/ losses. Most managers on the FX Desk in most companies lament this fact. There is a lot to anser for when a hedge goes out of money but there is nary a pat on the back when an exposure that has been purposely left unhedged goes into the money.

Clearly, there is a need for deep introspection within companies on this point. The FX Risk Manager seems to be the most hassled person in a company, in a constant danger of being crucified. Why?

QS 9. Are we willing to explicitly pay for Advice? Should advice be paid for separately from the commission/ brokerage payable on hedging transactions?

Lastly, very few companies recognise the benefits of divorcing advise from transactions.

Banks have tended to proffer free advise in order to attract companies to hedge through them. Companies, on their part have been happy to receive the free advise from banks. They are generally loath to pay explicitly for advice, not realizing that this is, in fact, the better option for them. Free advice has often played on the fear or greed of a Corporate, to induce it to hedge. The truth of this is borne out by the strange phenomenon of Corporate India as a whole selling Dollars at 40-41 in 2008, based on the advice that it would fall to 35.

Had companies sought independent advice, perhaps they might have been able to get an opinion to the contrary. Learning from experience, some companies have started to seek advise from independent, professional risk managers, instead of relying solely on the free advise given by banks. This is a step in the right direction, but there is still a long way to go.

Volatility can be tackled

Companies, especially in the manufacturing sector, routinely deal with the volatility in the prices of their raw materials as well as their final products. And they tend to do so successfully, turning in a neat net profit, year after year. Why then can they not deal with currency volatility, which is, in fact, much less than commodity volatility? What is needed is a proven method of tackling currency volatility. Such a method exists and is arrived at by introspecting on and answering the nine vital questions given above.

| 1 | "Developments in the Indian Rupee Market", Colour of Money, 22-Jan-09, by Kshitij Consultancy Services |

| 2 | "The need for focusing on the Currency Risk Management Process in the Corporate sector", Colour of Money, 16-Feb-08, by Kshitij Consultancy Services |

| 3 | "How paying Option Premium can actually be profitable". Colour of Money, 16-Feb-08, by Kshitij Consultancy Services |

You may also like:

In our last report (29-Jun-26, UST10Y 4.39%) we had followed the fall in Crude to $73 to change our US10Yr forecast from a rise to 5.10% by Sep-26 to a slight dip to 4.30% by Sep-26; and instead of the earlier forecast of a rise to 5.4% by Jan-27, the changed forecast projected …. Read More

In our June 2026 report (1-Jun-26, Brent @ $95.47), we had expected Brent to correct to $88 before bouncing back to $120 and $145 by Aug-26 and Sep-26, respectively. A sustained trade below $90 was said to be incumbent on a fully credible resolution of the US-Iran war. … Read More

In our June 2026 report (10-Jun-26, EURUSD 1.1546), we expected the Euro to rise towards 1.17 in Jun-26 before reversing lower, with surging crude prices, rising inflation, and potential central bank rate hikes posing key risks amid the ongoing US-Iran conflict …. Read More

In our last report on 03-Jun-26 report (10Yr GOI 7.03%) we remained bullish on Brent and therefore called for higher CPI and higher Yields. At the same time, we said, “Our view will come under threat if Brent trades … Read More

In our 10-Dec-25 report (USDJPY 156.70), we expected the USDJPY to trade within 154-158 region till Jan’26 before eventually rising in the long run. In line with our view, the pair limited the downside to … Read More

Our July ’26 Dollar Rupee Quarterly Forecast is now available. To order a PAID copy, please click here and take a trial of our service.