Indian IIP Growth

Aug, 15, 2013 By Vikram Murarka 0 comments

Indian IIP data for Nov-14 (+3.8% y/y) was released on 12-Jan-15. It has moved up smartly from the -4.2%. growth for Oct-14. But is that unequivocal good news? This report looks at the Indian IIP growth from a couple of other perspectives.

Growth? Or stagnation?

See boxes (1) and (2) in the chart alongside. For the last three years, the IIP Index has been ranging sideways between 194-163 and the annual growth rate between +6% and -4%, largely. Is this growth or stagnation?

The Index needs to rise past (3) or 180 at least if the growth rate is to move up to 5.9% at least. But (4) suggests there is trend resistance near the current levels

Further, we have to ask, even if the Industrial growth rate rises to 5.9%, is that good enough, given that India is looking to grow GDP itself at 5.9%? Industry probably needs to grow at least 8-10% if GDP growth is to move up to 5.9%. Recall, industrial growth was averaging 15-20% around 2007-08 when GDP was growing around 9%.

US growing faster than India

The chart alongside compares the industrial growth rate in India with that in the USA.

As can be seen, US grew 5.25% in Nov-14 as compared to India's growth of 3.8%.

Further, the USA has pulled itself out of the financial crisis and growth has not dipped below even 1% since 2010. Indian industrial growth, on the other hand, has been vacillating around the 0% level since 2011.

Seen on the same scale, (1) India averaged 15-20% in 2007-08, far outpacing the US growth of around 2% at that time. (2) But, Indian growth has been trending down since then whereas (3) US growth has been trending up.

Given that the US Industrial base is around 6 times that of India's, growth in India will have to be at least 6 times more than the US growth rate for India to attract huge amounts of capital.

From a domestic perspective, Indian Equities have gone up through 2014 on the hope and belief that the new Modi-government will be able to pull India out of its economic morass. While that is still a hope an belief, we have to see what rate of Industrial growth is already priced into the current level of the Sensex/ Nifty.

We would assume that the Equity market is pricing in around 10% industrial growth. Unless the IIP picks up strongly in the next few months, the markets could start coming off.

On the other hand, if the IIP does indeed rise past 6% in the next few months, Equities could shoot up.

But, while the market has moved up on hope so far, further rise from here will have to be backed by performance. That could be a tall order, going by what the numbers suggest at the moment and considering the growth slowdown dogging the global economy.

You may also like:

In our last report (29-Apr-26, UST10Yr 4.35%), we had said that the FED was likely to leave rates unchanged, which it did. We had also said that “once Kevin Warsh comes in, the FED is more likely to cut, responding to …. Read More

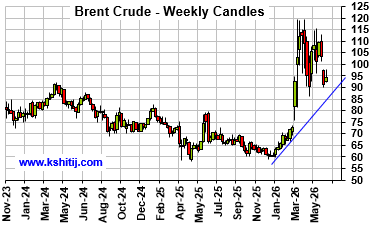

In our May 2026 report (4-May-26, Brent @ $110.75), we expected Brent to test $90.50 by Jul-26, followed by a rise to $145.13 by Sep-26 and $161.93 by Dec-26. Sustained trade below $100 was expected to be seen only on a credible resolution of the US-Iran war, which looked unlikely … Read More

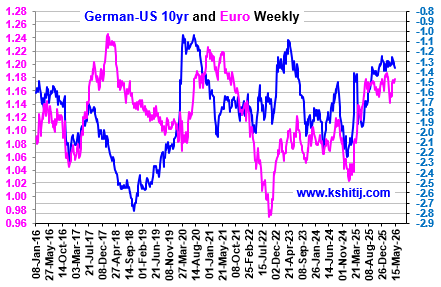

In our April 2026 report (13-Apr-26, EURUSD 1.1686), we expected the Euro to rise to 1.1950 by May-26 while retaining our long-term bearishness towards 1.10 by Aug’26. The main reasons were good chances of a rise in the Dollar Index and crude prices. The markets expect the ECB to move. …. Read More

In our 11-Apr-26 report (10Yr GOI 7.03%) we had retained our bullish view on Brent towards $134 by Sep-26, while allowing for a near term dip to $95 on hopes of a US-Iran resolution. Brent fell to $89.93, lower than … Read More

In our 10-Dec-25 report (USDJPY 156.70), we expected the USDJPY to trade within 154-158 region till Jan’26 before eventually rising in the long run. In line with our view, the pair limited the downside to … Read More

Our May ’26 Dollar Rupee Monthly Forecast is now available. To order a PAID copy, please click here and take a trial of our service.